«Upstream» and «downstream» are general business terms referring to a company›s location in the supply chain. The closer to the end user a function or firm is, the further downstream it is said to be. Raw material extraction or production are elements of the supply chain considered to be upstream. The oil and gas supply chain is commonly referenced in this manner. The upstream companies identify oil and natural gas deposits and engage in the extraction of these resources from underground. These firms are often called exploration and production companies. Refiners represent the downstream element of the oil and gas supply chain.

Downstream operations include refineries and marketing and commonly refers to the refining of petroleum crude oil and the processing and purifying of raw natural gas, The downstream sector touches consumers through products such as gasoline or petrol, kerosene, jet fuel, diesel oil, heating oil, fuel oils, lubricants, waxes, asphalt, natural gas, and liquefied petroleum gas (LPG) as well as hundreds of petrochemicals. Marketing services help move the finished products from energy companies to retailers or end users. Some of the products commonly associated with the Downstream sector include: Liquified Petroleum Gas (LPG); Liquefied Natural Gas (LNG); Gasoline; Diesel Oil; Jet Fuel; Heating Oil; Other Fuel Oils; Propane; Asphalt; Synthetic; Rubber; Plastics; Petroleum Coke; Lubricants; Pharmaceuticals; Antifreeze; Fertilizers; and Pesticides.

Investments in downstream in emerging markets generally carry higher risks than similar investments in developed countries. Factors related to emerging market operations that can threaten production or profitability for oil companies include infrastructure problems, labor problems and maintenance problems. Along with all the usual risks associated with any investment, operations in emerging markets are subject to specific additional risks. This is particularly true for oil companies, since they typically have large amounts of capital invested in their operations and also because they have to deal with a larger number of issues as compared to some other types of businesses.

One of the major problems for oil companies operating in emerging market nations is the lack of a highly developed infrastructure. Oil companies usually have to fund road, water and electricity access to drilling sites. This can require a much greater expenditure of time and money than it usually does in developed countries. Additionally, infrastructure maintenance tends to be unreliable and less well-established. An additional problem somewhat related to infrastructure problems may arise in the form of difficulties and extra expenses related to acquiring necessary equipment and replacement parts in a timely manner.

Potential labor problems include a lack of skilled workers. Workers may have to be transported over long distances or housed at the operations site.

Legal and regulatory issues can be problematic as well. Oil companies have to negotiate a number of legal contracts and they must deal with government and local regulations. These issues are obviously more difficult to deal with in a country where the company is less familiar with the applicable laws and regulatory requirements. These issues can increase costs or even threaten to shut down operations.

Shipping costs, including tariffs and various import/export expenses, may increase overall operational costs significantly. Similarly, political uncertainty and foreign currency exchange risks are also inherent for any company doing business in a foreign country.

The downstream industry, on the other hand, follows a different business model. It›s not as capital intensive as the upstream industry, and its operations work with variable costs. This kind of industry will surely show a much lower EBITDA (Earnings Before Interests, Tax, and Depreciation & Amortisation). However, operating profits may be just fine. This kind of industry also has another characteristic: it deals with a huge amount of money in transactions, and depends on how you handle these transactions, bottom line numbers can vary a lot.

Global Refining Industry: Winds of Change

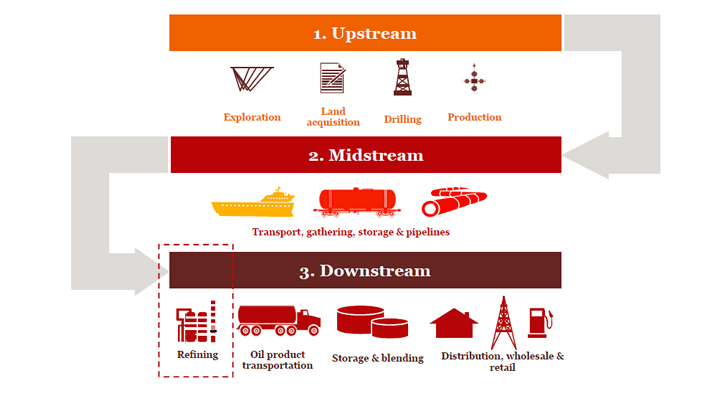

The petroleum value chain can be divided into three sectors: upstream, midstream and downstream. Upstream and downstream activities all have a direct impact on refining activity and economics.

Crude Acquisition and Transportation:

Crude is produced or purchased, and transported to the refinery gate. Crude oil can be transported by pipelines, cargoes, barges, rails and trucks. Pipelines and large cargoes are the most cost effective means of transport over very long distance, whereas barges, rails and trucks are used for shorter distance and for where pipelines or ships are not available.

Refining:

Crude oil and other feed stocks are distilled, converted and treated during the refining process to produce a range of petroleum products such as LPG, naphtha, gasoline, diesel, jet/kerosene, fuel oil, asphalt/bitumen, waxes, etc. These find end uses as transport fuels, power station fuels, heating & cooking oils, chemical feed stocks, road paving substances, etc.

Primary Distribution:

The various petroleum products are transported from the refinery storage / blending tanks via pipelines, road tankers, railcars, barges to storage tank terminals where product blending takes place to meet certain product specifications (called ‘rack blending’). Some products such as chemical feed stocks, fuel oil, and asphalt are delivered directly to industry customers.

Secondary Distribution:

Products are delivered to wholesale customers (e.g. jet fuel, gasoil) or retail customers (e.g. LPG, gasoline, diesel) via trucks. For transport fuel products (gasoline, diesel), small quantities of biofuels or unique additives can be added into the delivery trucks. Additives are used to make ‘premium fuels’, which increase engine performance, lifetime, clean combustion etc.

Retailing:

Retail fuel products are transported to petroleum service stations (i.e. forecourts) where commercial and private vehicles can be fuelled up. Many service stations also have other vehicle services (e.g. car wash, lube change) and convenience stores, food courts to accumulate additional earnings. Stations can be manned (staffed) or unmanned (self-serve).

With the exception of the US Gulf Coast, global refining fundamentals are currently weak

Global: With a couple of exceptions, the global refining industry is living through a sustained period of poor margins. This is driven by demand weakness and a continued supply overhang. On the demand side, sustained gasoline demand contraction in mature economies and weak growth in emerging markets, notably Asia are on-going. On the supply side, Europe and Asia are struggling to correct overcapacity, whilst the US demand contraction is resulting in increased length. Fundamentals are weak.

US West Coast: Current gasoline and distillate surplus is keeping refining utilisation and margins low. In addition, Canadian crude pipeline permitting delays and a much stronger industry response to the heavy coking margin weakness resulting in slower light tight oil (LTO) penetration than in other parts of the US.

North West Europe: A failure to close sufficient refining capacity is resulting in low margins. Margin downside pressures remain, including demand contraction (due to vehicle efficiency, biofuels and high oil price) as well as competition from imports from advantaged regions (notably Russia, ME and increasingly US).

US Gulf Coast: USGC is currently enjoying margin support from discounts in LTO (i.e. lower priced feedstock than USWC or NWE). Margins are strong. However, overall road fuel demand continues to decline.

Asia: Current margins are depressed by refining overcapacity and recent slow demand growth. Demand outlook is not as strong has over the last 10 years. The continued addition of high complexity new refining capacity is likely to result in a sustained capacity overhang

Demand Shifts towards Developing Economies

The global refining industry is currently undergoing significant fundamental shifts in both demand and capacity.

- Global oil product demand continues to grow but has shifted from developed economies (North America, Europe, Japan) to developing economies (Asia, Latin America, Middle East, Africa).

- Demand growth in developed regions remains stagnant or declining due to sluggish economic growth, high product prices, higher vehicle efficiency reducing consumption, and increased penetration of alternative fuels (biofuels, gas) and of electric vehicles.

- Growth in developing / emerging markets is still supported by economic and population growth, increased mobility and power needs, higher energy consumption per capita, and fuel subsidy programs; however signs of economic growth slowdown in countries such as China, India may impact short to medium term demand.

- Rising demand for gasoil/diesel will be the key growth driver with modest growth forecast for gasoline and other light end products (LPG, naphtha, gasoline, jet) while fuel oil consumption is expected to drop further.

- The shift to higher fuel quality standards worldwide in line with environmental regulations means the industry needs to meet the increased demand for higher quality products (e.g. lower sulphur), requiring additional capital investment and higher operating cost.

Capacity Shifting to Match Demand

- As consumption moves to new geographies, new capacity has been added to meet this growth, adding to refining overcapacity globally.

- Less advantaged refineries (lower efficiency, subscale, low complexity, more expensive feed stocks) are becoming more vulnerable to increased competition from more, and better advantaged export refineries.

- In particular, European refineries have struggled to compete with the influx of export refineries in the Middle East and Asia (e.g. India) for quite some time, and recently also from the US. This has resulted in poor margins and ongoing capacity closures / rationalisation in Europe, albeit at a slower pace than required.

- The focus in the future therefore will be addressing this refining overcapacity while rebalancing some product demand (i.e. more diesel and less gasoline).

Unconventional Oil and Further Changes in Market Dynamics are Forcing the Industry to Adapt

Unconventional oil in the US has had a significant impact on US liquids production:

- Trade flow and margin shift.

- The rapid growth in tight oil production, mainly in the US, and unconventional heavy oil sands production in Canada have had a profound impact on:

- Global oil prices (e.g. widened WTI-Brent price differentials, narrowed light/heavy differentials).

- Global oil trade movement (e.g. displacing US crude imports from West Africa and Latin America, increasing possibility of US crude oil export).

- Product trade movement (e.g. more gasoline & diesel products exports from the US, European gasoline exports redirected to Africa and Latin America)

- Refinery margins (e.g. higher margins for US refiners at the expense of margins in Europe and Asia).

- Anticipated strong unconventional production growth in the future will continue to influence and challenge the refining industry globally, leading to further restructuring and rationalisation.

Crude supply mix continues to change:

- The proportion of crude oil that needs to be refined per barrel of incremental product continues to decline, as the total share of biofuels, GTLs, CTLs, NGLs and other non-crudes continues to rise, which present different product yields.

- Refiners will also need to continue to adapt to changes in crude supply sources, volume and quality (i.e. Light – heavy, sweet – sour) of the current supply outputs as well as other new crude streams coming on stream.

Developing economies are expected to account for all oil product demand growth in the future, offset by falling demand in developed economies in North America & Europe.

- Global oil product demand increased by 1.4 mbd (million barrels per day) in 2013, a strong rebound compared to the 2011 – 2012 growth levels and 10-year historical average.

- OPEC has projected global demand to grow from 89 mbd in 2012 to 108.5mbd in 2035, representing a growth of 0.9mbd or 0.9% per year.

- Developing economies are expected to account for all refined product demand growth to 2035, led by China and other Asia Pacific countries.

- This expectation is being supported by the increased fuel demand in the transport and power sectors, fuelled by robust economic growth, fuel subsidies and rising energy consumption per capita.

- Declining product consumption in Europe, North America, and Japan is forecasted to continue due mainly to falling fuel demand for transport coupled with sluggish/negative economic growth.

- Ongoing reduced transport fuel consumption has been driven by vehicle fuel efficiency, increased use of hybrid and electric vehicles, and increased alternative fuels such as natural gas and biofuels.

Demand for Middle Distillates Is Likely To Drive the Majority Of Growth, Followed By Gasoline And Other Light End Products

- Demand for diesel/gasoil in the transport sector will be the key driver of growth globally out to 2035.

- Diesel/gasoil demand is expected to jump by >10mbd between 2012- 2035, or >50% of total refined product growth in that period.

- This is fuelled by expansion in both commercial fleets (buses, trucks, light duty vehicles) and diesel passenger cars.

- Contributing to this growth are the changes in marine fuel quality specifications in 2015 and 2020 which will introduce significant shift of fuel oil usage into gasoil.

- Increased mobility and energy requirement will drive future demand for other light-end products such as LPG, gasoline/naphtha, jet fuel while demand for ‘domestic’ kerosene (used in lighting, heating, cooking) and fuel oil (used in power generation, fuelling ships) will fall.

Despite weak fundamentals, global refining capacity continues to expand, led by Asia Pacific and the Middle East.

- Global refining capacity increased by 1.4mbd in 2013, compared to 1.3mbd in 2012 and 0.4mbd in 2011

- 2013 capacity additions mainly took place in China and the Middle East, accounting for 0.7mbd and 0.6mbd of additions respectively.

- Smaller expansion has also been seen in Africa, Russia, and South America.

- Offsetting this development is the continued capacity contraction in Europe due to weak product demand, depressed margins and increased export competition from elsewhere.

- Nevertheless slower than expected demand and anticipated overcapacity in Asia has reigned in Chinese capacity growth, signalled by the postponement of some new refinery start-ups and expansion plans (e.g. Petrochina, BP in China).

- The global trend towards larger and more complex refineries has seen a reduction in number of refineries despite capacity growth.

Future refinery capacity development is likely to reflect the demand shift from developed to developing regions.

- Refinery capacity outlook will continue to reflect the product demand shift, i.e. from mature markets to emerging economies where most if not all of product demand growth will take place.

- Prolonged low margin pressure will result in more European closures over the next few years, whereas continued capacity additions in Asia in a weak margin environment will force refiners to run at reduced rates or delay expansion projects.

- Accelerating production of unconventional oil (light tight oil in the US and oil sands Canada) will dramatically change the global crude trade flows, crude and other feedstock prices, which in turn have significant impact on product trade flows and prices. This will lead to further restructuring and relocation of the global refining sector.

About PwC

PwC helps organizations and individuals create the value they’re looking for. We’re a network of firms in 157 countries with more than 195,000 people who are committed to delivering quality in assurance, tax, and advisory services. Find out more and tell us what matters to you by visiting us at www.pwc.com PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

DR. AHMED RASHWAN

PwC Director- Head of Oil & Gas

BASMA SAMRA

PwC Partner- Utility, Mining & Energy Leader

WAEL SAKR

PwC Partner-Assurance Leader

HISHAM OWIS

PwC Director, Industry Expert