The Strait of Hormuz remains the world’s most consequential energy chokepoint, a narrow waterway that functions as the beating heart of global commerce. In 2024, this vital artery carried roughly 25% of all seaborne oil and 20% of global Liquefied Natural Gas (LNG) flows-a staggering volume that anchors the world’s energy security. Following the February 28 US and Israeli strikes on its leadership and facilities, Iran has turned the Strait into a high-stakes geopolitical weapon. Bordering the northern side of the passage, Tehran exerts significant control over shipping through the waterway due to its proximity to primary lanes and its robust military presence. By leveraging these factors, Iran has effectively throttled the waterway through ship detentions, navigational interference, and sea mines, restricting transit almost exclusively to Iranian-flagged vessels.

Regional and International Counteractions

These retaliatory measures have forced Gulf neighbors to shut down wells as storage hits capacity, while Qatar has entirely suspended its LNG production. In a desperate bid for stability, Saudi Arabia is diverting exports through inland pipelines as the International Energy Agency (IEA) coordinates a global release of strategic reserves. Yet, a striking irony remains: while regional exports have plummeted, Iranian crude continues to flow at a near-normal pace. Data from maritime intelligence firm TankerTrackers.com shows that Iran has successfully exported roughly 13.7 million barrels (mmbbl) since the conflict began, according to Reuters. Despite this steady Iranian flow, market anxiety persists; Brent crude remains anchored near $100 per barrel, and with LNG prices soaring, the global energy landscape remains in a state of high-priced paralysis.

Inland alternative routes

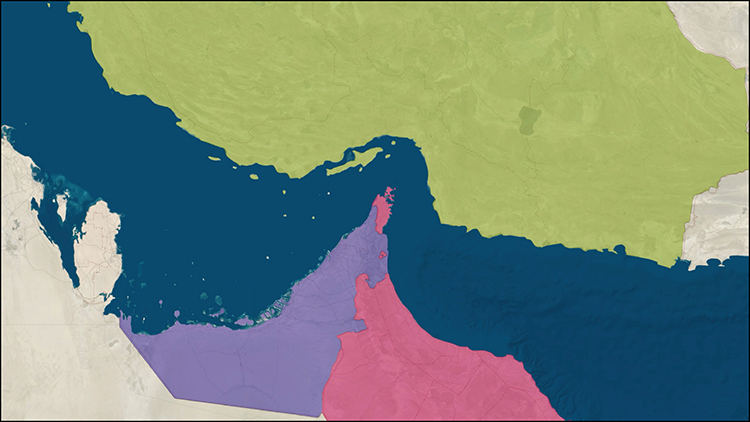

Gulf countries are increasingly utilizing strategic bypasses to move their product. Saudi Arabia’s East-West Pipeline, or Petroline, serves as a high-capacity lifeline capable of shunting 5 million barrels per day (mmbbl/d)-representing over 75% of the Kingdom’s projected 2025 exports-away from the Gulf and toward the Red Sea port of Yanbu. Notably, the capacity of this pipeline was expanded to 7 mmbbl/d in 2019. Meanwhile, a 1.8 mmbbl/d pipeline transports crude oil from Abu Dhabi’s inland fields to Fujairah, which sits safely outside the Strait of Hormuz. “These routes represent more than just infrastructure; they are the regional powers’ definitive hedge against a closed Strait, ensuring that global energy flows can pivot even when the gates of Hormuz are under pressure”, according to Capital Economics, a UK-based think tank.

Red Sea Threats

Recent developments have sharpened a central geopolitical question: will Tehran permit Saudi Arabia to continue exporting crude through Yanbu without attempting to interfere? According to the Middle East Economic Survey (MEES), an energy industry publication, Yemen’s Iran-backed Houthis may be emboldened to resume attacks on vessels in the southern Red Sea, effectively closing-once more-the Bab al-Mandeb chokepoint. Oil tankers carrying Saudi crude bound for Asian markets must navigate this narrow passage, making it a critical vulnerability in the Kingdom’s export strategy.

Suez Canal and SUMED Options

If the Bab al-Mandeb were to be shut, Saudi Arabia would have limited alternatives and would likely be forced to reroute its crude shipments north toward the Suez Canal and Egypt’s SUMED pipeline, which links the Red Sea port of Ain Sukhna with the Mediterranean terminal at Sidi Kerir. Indeed, in early March, Egypt’s Minister of Petroleum and Mineral Resources, Karim Badawi, stated that Cairo stands ready to facilitate the transfer of Saudi crude from the Red Sea to the Mediterranean via the SUMED Pipeline. However, the logistics of such a shift are complex.

Fully loaded Very Large Crude Carriers (VLCCs) cannot transit the Suez Canal, which forces them to discharge part of their cargo at Ain Sukhna before continuing the journey. Saudi Arabia’s reliance on the SUMED route typically involves VLCCs shuttling crude between Yanbu and Ain Sukhna, where the oil is offloaded, transmitted through the pipeline, and then reloaded onto other tankers at Sidi Kerir for onward delivery.

While this appears to be a viable solution, this route primarily facilitates sales into European markets across the Mediterranean, whereas the majority of Saudi oil is marketed in Asia.

The MEES report noted that the only exit from this dilemma would be for tankers to load cargoes at Sidi Kerir, exit the Mediterranean, and sail around the southern tip of Africa to reach Asia-a journey that would take considerably longer and involve significantly higher costs.

Even if enough buyers were willing to accept this option, Ain Sukhna itself represents a logistical bottleneck. The SUMED pipeline has the capacity to handle up to 2.5 mmbbl/d of crude oil flows, which is just half of what Aramco hopes to export from Yanbu. This is not the whole picture, as crude from other Gulf producers lacks even this flexibility. Unlike Saudi Arabia and the UAE, most oil flows originating from Iraq, Kuwait, and Iran cannot be rerouted. As a result, a Capital Economics report highlighted that somewhere between 10–20% of global oil supplies could end up trapped.

Trapped LNG Supplies

Regional LNG flows face even steeper challenges, as they cannot be diverted. The absence of alternative routes explains why the European Title Transfer Facility (TTF) natural gas benchmark has registered sharper increases than Brent crude. The TTF is a virtual trading hub for natural gas and serves as Europe’s leading benchmark for wholesale gas prices, much like Brent does for oil. Two weeks into the conflict, TTF prices had surged by about 60% to €50–52 per Megawatt-hour (MWh), while Brent crude rose roughly 30–35%, moving from $75–80 per barrel to approximately $100–102 per barrel as of March 14.

Most LNG shipments passing through the Strait originate from Qatar, a dominant player in the global market, while nearly 40% of the crude oil transiting Hormuz-around 5.3 mmbbl/d-comes from Saudi Arabia. Overall, 80–90% of the crude and LNG flows through the Strait are destined for Asia. China stands as the largest buyer, importing both Iranian oil and other crude passing through Hormuz. Combined, these volumes amount to about 5.4 million barrels per day, representing just under half of China’s total crude imports. This gives Beijing significant leverage and a profound interest in ensuring uninterrupted energy trade.

The Price of Volatility

As markets priced in the growing risk of Middle Eastern conflict, oil prices had already climbed approximately 15% this year, reaching about $72 per barrel prior to the latest military strikes, according to Capital Economics. In the most benign near-term scenario, the firm anticipates a geopolitical risk premium of roughly $10–15 per barrel being added to the baseline cost.

A broader regional conflict would naturally catalyze a wider range of potential outcomes. In a middle scenario, persistent hostilities would keep risk premiums elevated without necessarily causing a major disruption to actual physical supply. Under these specific conditions, analysts expect that oil prices could remain stabilized within the $70–80 per barrel range for an extended duration. However, in a more severe scenario-one where energy flows face sustained and significant disruptions-crude prices could realistically climb above the $100 per barrel threshold.

The impact extends significantly beyond oil into the global gas markets. If Qatari LNG exports were to be disrupted, European TTF natural gas prices could surge to approximately €80–100 per MWh. While such a spike would represent roughly double current price levels, it would notably remain well below the €200-plus peaks recorded in the third quarter of 2022 following the invasion of Ukraine.